Taxes: One of those questions we’d rather ignore.

And yet somewhere the phrase “quarterly taxes” has come up.

Wait, what?

For bloggers, podcasters, Youtubers and others who are self employed and make money from their content, it’s bad enough to have one tax time. But now we’re adding four more?

This can’t be right. It can’t be fair!

Do we have to file quarterly taxes if we’re making money because of our content creation?

I have good news for you. Quarterly taxes are not a thing.

However, sending in quarterly tax payments may be a thing for you, depending on your personal tax situation.

We’ll wade through all the terminology like quarterly taxes, estimated tax payments, or whatever you want to call it. We’ll discuss the following questions:

- What exactly is this quarterly thing all about and how does it impact bloggers, podcasters, YouTubers and other content creators?

- Are quarterly payments required?

- How do we know how much to send in?

- When are the quarterly tax payment dates?

- How do content creators like bloggers, podcasters, and Youtubers file quarterly taxes?

Is this article for you?

Before I go any further, let me clarify something: This is about taxes for the self-employed. If your digital business is making a profit (bringing in more money than it costs to operate) you’ll be taxed like a business. Technically, you’re running your own business. Even if this is just a side hustle.

Most of us pay taxes for our business on our personal tax return. If you’re filing as a sole proprietor, independent contractor, or even a single member LLC, it’s all part of your individual income tax process. Maybe you’ve already paid taxes for the previous tax season and you remember something about a Schedule C. This article is for you.

If you’re not sure, chances are high that this article is for you as well. Maybe you just recently started receiving enough income to even think about it, but you haven’t looked further into it. Most likely you’re in that sole-proprietor category (usually you’d know if you did something different).

However, if you have incorporated your business (such as creating a C or S Corporation) or set up your LLC so it’s taxed like a corporation, there are enough things that are different about your quarterly taxes, and this article may not be as helpful.

One more thing I should make clear: This is not tax advice. I am not a tax professional. The purpose of this article is to provide general information about how taxes work for self-employed content creators. Your tax situation is different from anyone else’s. If you need tax advice for your personal circumstances you should seek out a tax professional.

What exactly is this quarterly thing all about and how does it impact bloggers, podcasters, YouTubers and other content creators?

I’ll repeat what I said earlier. Quarterly taxes are not a thing. That’s because as self-employed small business owners, taxes associated with our business income are filed with annual income taxes.

But let me repeat: There is no additional tax that’s filed quarterly. We don’t even report our income or expenses quarterly. That’s only done once a year.

While many call them ‘quarterly taxes,’ they’re actually simply quarterly estimated tax payments. I would go so far as to say you’re not actually filing anything. You are simply sending in a payment each quarter.

The best way to put it is that quarterly estimated tax payments are our way to withhold and submit our tax payments throughout the year. When we are self-employed, obviously no one is taking our taxes out for us, so it’s up to us.

Keep in mind that this is about federal income and self-employment taxes. Some state or local taxes may be different. You will need to look up dates and requirements for your state and local governments.

Also remember that this article refers to income taxes. Sales taxes, payroll taxes, property taxes and other types all have their own rules.

Are quarterly payments required?

There is no specific requirement that every business needs to make quarterly payments. In the end it’s a judgment call you need to make based on your tax situation.

If you have reason to believe you will have to pay in on your personal tax return, it’s a really good idea to make quarterly payments.

The requirement here isn’t about making quarterly payments. It’s about making sure that most of your taxes have been paid up by the end of the year.

The U.S. tax system operates on a pay-as-you-go basis. This means that taxpayers need to pay most of their tax during the year, as the income is earned or received. Taxpayers must generally pay at least 90 percent (however, see 2018 Penalty Relief, below) of their taxes throughout the year through withholding, estimated or additional tax payments or a combination of the two. If they don’t, they may owe an estimated tax penalty when they file.

IRS Basics of estimated taxes for individuals

THAT is the requirement here. “Taxpayers need to pay most of their taxes during the year, as the income is earned or received.”

If you haven’t paid in enough by April 15 (or whatever tax day is for the year), you may “owe an estimated tax penalty” when you file.

We are not required to make quarterly payments for the sake of making them. Rather, if you do have to pay in on tax day (typically if you have to pay more than $1,000) then you’ll have to pay extra in penalties and interest.

Your quarterly payments are your way of making sure the payments have been submitted and avoiding those extra fees.

Ultimately, it’s a judgment call on your part.

Does that mean that quarterly payments are optional?

I don’t know that I’m going to go that far. It’s not as much about required verses optional. It’s really more about whether it’s the best practice for you.

This is not like not filing your annual income tax return where there a major problems if you fail to file. The Internal Revenue Service isn’t going to hunt you down if you didn’t send in a quarterly payment.

The reason I wouldn’t call it optional is that if you do have to pay in on tax day, you may have to pay in extra because you didn’t make that payment. It’s hard to call that optional.

Here’s what it boils down to: If you won’t need to pay in on April 15, you won’t need to make quarterly payments. That could mean:

- You didn’t make enough money to owe taxes

- You had enough tax credits to cover your taxes for your business profits

- There was enough withheld from other income sources (such as your or your spouse’s W2 income) to cover your taxes.

If you don’t need the quarterly payments to cover your end of year tax liability then quarterly payments aren’t required. If you do, sending the quarterly estimated payment will avoid penalties and interest.

How do we know how much to send in?

You send in what you send in.

Maybe that’s too glib. But it’s glib for a reason. I think we get freaked out about quarterly taxes, and we don’t need to be.

Let’s face it: when you start looking into it, it’s kind of intimidating. It actually looks a bit complicated. Who needs all that extra complication four more times a year?

But the thing is, it’s not as complex as it looks. I’ll get into that more in a bit.

There are no hard and fast rules about how much to send in. It’s as simple as paying enough to make sure you won’t owe money on April 15. How you determine that amount is completely up to you.

I’m glib because I don’t want you to be afraid of this. You don’t have to get this perfect. Not even close. There’s no audit to worry about, no IRS thugs are coming after you if you get it wrong. This does not need to be precise.

First priority is make sure you’re paying enough.

An optional second priority is to avoid paying too much in. But if that interferes with priority #1, remember which priority is first. There’s no damage if you send in too much, you’ll just get it back in your tax refund. I just say that because I’m not a fan of giving Uncle Sam an interest free loan.

Here are some steps you can take:

1. Understand what self-employment income is taxable.

I think a lot of content creators and digital entrepreneurs get scared of this one. But there’s some good news here.

You get all that money from affiliate marketing, YouTube advertising, sponsorship and ads, influencer payments, products, online courses, and so many other things. You get a little scared when you start adding it up.

However, your taxes are based on your business profit. In other words, your taxable income is what’s left over after expenses. That’s a lot less daunting than paying on everything that comes in.

Hosting fees, plugins, services, equipment for your business. All of the things that are necessary and ordinary for operating your business. Your taxes are based on what’s left over AFTER your business expenses.

We’re not going to get into all the details here. That’s a whole different topic. But you can go through all the things you have to pay out to create your content and get an idea what those expenses are.

2. Understand these basics about taxes.

There are actually two taxes at play here.

Income tax and self-employment tax.

Income tax could be nothing. It could be a third or more of your profits. It all depends on tax deductions, credits, dependents and all that stuff.

If your business is your entire source of income, only part of your income will be subject to income tax. If you have substantial additional income, every dollar may be taxed and at a higher percentage.

Self-employment tax is our version of FICA / Social Security / Medicare taxes. It is 15.3% of every dollar of profit your business profits.

This is the one that sneaks up on us. There are a few reasons for this:

- We don’t usually think about this one when we think of taxes because we’re not accustomed to filing tax forms. When we’re employees, that money is just taken out and there’s nothing more we have to do.

- Self-employment tax is charged against every dollar of profit. Just like FICA, it starts with the first dollar. Income tax deductions and many tax credits do not apply here. You could have zero income taxes and a huge self-employment tax bill.

- We pay double what we would pay as an employee. That’s because an employer pays half of the total. You’re your own employer, so guess who gets to pay that other half?

Having an idea of what your tax rates look like gives you a better idea how your business profits will impact your total taxes. That helps you determine what to pay in each quarter.

3. Determine how you will estimate what to pay in.

The Internal Revenue Service recommended best practices include making estimated tax payments in equal amounts in order to avoid a penalty.

Generally, taxpayers should make estimated tax payments in four equal amounts to avoid a penalty. However, if you receive income unevenly during the year, you may be able to vary the amounts of the payments to avoid or lower the penalty by using the annualized installment method.

IRS Topic 306 Penalty for Underpayment of Estimated Tax.

If you expect that your income will be fairly steady from one quarter to another, it’s best to try to calculate your total tax payment for the year and then divide by four.

For a lot of us who are just starting to ramp up our businesses, it’s hard to determine what the money will be like from quarter to quarter. A lot of time once the income opportunities begin, they just blow up. If income grows unexpectedly, just figure it out on a quarter by quarter basis. In that event, you may have to add a form when you file taxes that shows your income on a quarter by quarter basis.

There are a number of ways you can decide what to put aside.

Set aside a flat percentage.

This may be the simplest method. You could do this either based on the gross earnings (total money received) or based on the profit. I lean towards using profit, though that does require keeping up on some form of bookkeeping.

With 15.3% self-employment taxes assessed on every dollar of self-employed profit, that profit isn’t going to fluctuate based on how much you earn. That makes 15% a good starting point.

Then you want to figure out a percent to cover federal income tax. You could play the safe route and figure out your tax bracket and use that. Multiply your profits for the quarter by four and compare that to the federal tax brackets. For instance, If you have $5,000 profits for the quarter, that’s a pace for $20,000 annually, which is in the 12% tax bracket.

In that situation, 12% income tax is 15.3% self-employment is 27.3%. That’s likely going to be a bit high, so you could go with 25% of your profits.

Use a tool from a third party app.

Some bookkeeping apps have good tools for estimating quarterly taxes. Quickbooks Self Employed is a popular accounting software for sole proprietors. Hurdlr has a great free app for expense and mileage tracking and also has a subscription version with more features (this is an affiliate link, meaning I may receive a commission if a purchase is made from it).

Here’s a walk through that I do using the free version of Hurdlr to do a quick estimate of quarterly taxes:

As you enter your income and expenses, they will provide an estimate of what the tax impact is of your business profits. Programs like Quickbooks Self Employed and Hurdlr walk you through a tax profile where you enter your filing status, additional income, etc. Then as you update expenses and income, the program will adjust their estimate of the taxes you will need to plan on.

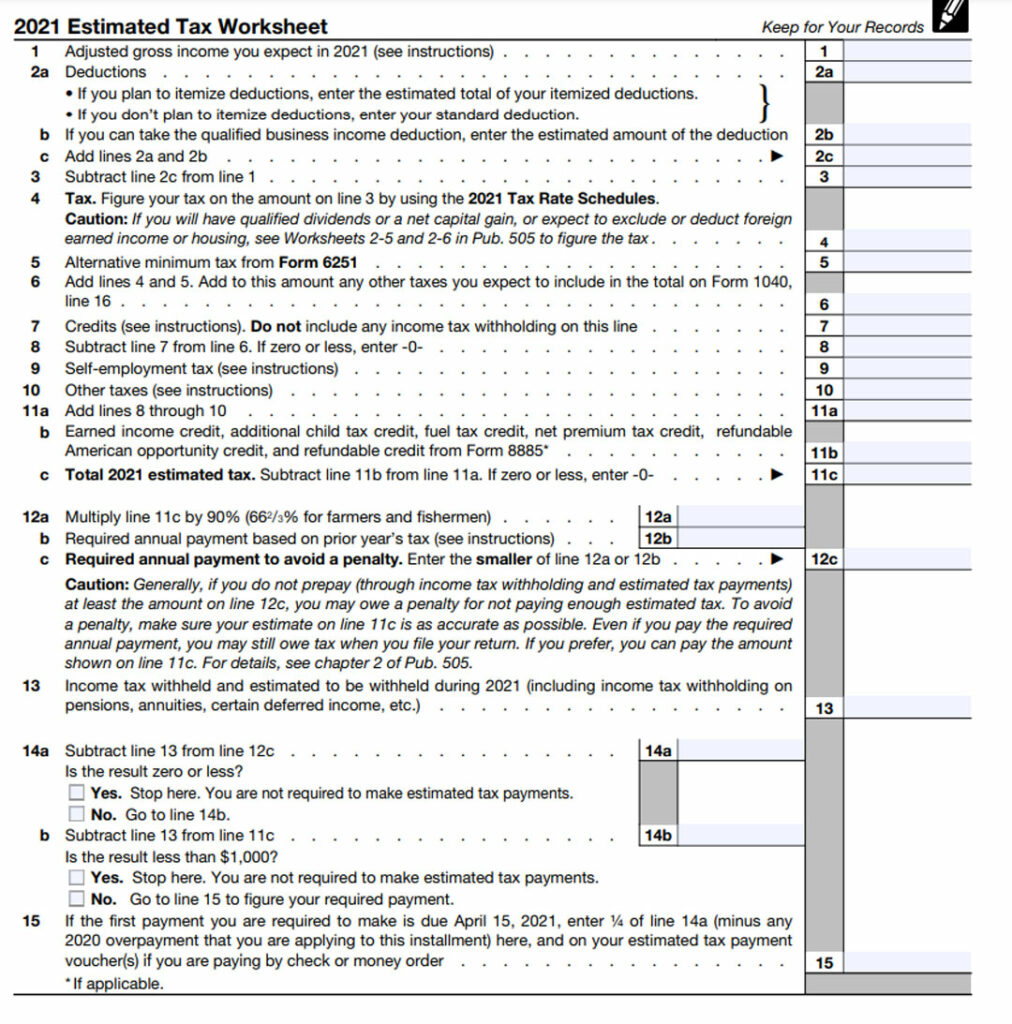

You can always try the IRS’s tool.

Good luck with that.

You can go to The IRS form 1040-ES pdf and find the estimated tax worksheet.

If you’re good at circular instructions that bounce you around and confuse most mere mortals, go for it.

The first time I ever went to send in a quarterly payment, I thought I had to do the worksheet. I always think I’m pretty good at this kind of stuff but my eyes glazed over pretty quick.

Basically you’re estimating your total 1040 tax return. It starts off asking what you think your Adjusted Gross Income will be for 2021. In other words, there’s a lot of extra home work (and studying) you have to do to figure out how to do that.

Here’s what I’ve done.

Personally, I’ve used the first option. I would do a very quick estimate of my profits, and then I would save 20% of that. I based that on what my payments ended up being the first time I was self employed.

Now this worked for me because my income was fairly steady from year to year. There weren’t any huge fluctuations.

The first year, I went with a higher percent. For the first three quarterly payments, I was setting aside 25% of my profits. Then in early January, I did an early run of my taxes (based on estimates on a lot of things since a lot of forms hadn’t come in yet).

Then, I could take what the estimated tax bill was and compare it to withholding from W2 jobs, the estimated payments sent in, and any tax credits we believed we’d get. By then I could get a good idea what that final total was, and for the 4th quarter payment (January 15) I could just send in the difference.

Whichever method you choose, the main objective is to send in enough that you don’t have a tax bill when you file. That avoids the extra fees.

4. Set the money aside on a regular basis.

Put that money aside into a savings account as soon as it comes in. It really works best to put it in a separate account. That makes it a little tougher to touch it or raid that money.

5. Send it in each quarter at the quarterly due date

That’s what we’ll talk about next.

When are the quarterly tax payment dates?

Every quarter, right?

Yeah, the IRS doesn’t seem to believe in logic.

April 15 makes sense. That’s a couple weeks after the first quarter ends.

So then July and October would make sense as well, right?

The quarterly due dates are:

- 1st Quarter = April 15

- 2nd Quarter = June 15

- 3rd Quarter = September 15

- 4th Quarter = January 15.

Whyyyyyy?

The answer I find is that it’s a typical government thing. At some point the government decided they wanted to get the 3rd quarter payments before the end of September because that was the end of the fiscal year. You know how it is, we have a choice between not spending the money or sucking up some of next year’s money into this year’s budget.

And then for some reason, they decided that since October changed, they needed to change another month. So now we have July’s payment in June.

The best thing I can say is, it doesn’t help much to try to figure it out. It is what it is.

How do content creators like bloggers, podcasters, and Youtubers file quarterly taxes?

As I mentioned above, the worksheet made it look very intimidating.

But when you look at what’s actually involved, sending in your quarterly payment is pretty easy.

The quarterly tax form you send in is pretty simple. It pretty much involves two things:

- Who are you?

- How much are you sending us?

That’s pretty much it.

Most of it involves entering your personal information. Name, address, social security.

And then you enter the amount that you’re sending in the box on the top right, and mail it in with your check.

Okay, no one sends a check any more, do they? The IRS does have an online portal, where you can pay with your bank account routing number and account number, or you can use a credit or debit card for an additional fee. It’s not the most intuitive thing. In fact I found two different portals. However the IRS seems to indicate the EFTPS portal that I linked to is the best option.

And there you have it. It’s not the most intuitive thing and yet when you get down to it, filing is as simple as it gets. That’s government work for you. We’ll summarize some of the above points with these FAQ’s.

Frequently asked questions about quarterly tax payments.

Do I have to file quarterly taxes as a self employed entrepreneur or content creator?

No. You only file your annual income and self-employment taxes.

So then, what are the quarterly tax payments?

Quarterly estimated tax payments are simply your way of withholding taxes from your income as a self employed person and of submitting those payments. It’s a way of pre-paying your taxes for the current tax year.

Will I be in trouble for not sending in quarterly payments?

You do not need to worry about quarterly estimates or payments if you won’t owe money on your taxes. You won’t get “in trouble” for not filing. If you do end up owing money when you file your annual taxes and did not send in enough through the year for estimated payments, you may have penalties and interest added to your tax bill.

What if I get the amount wrong?

There is no set amount. Ultimately it’s your responsibility to pay as you go, however it’s also up to you to estimate what the right amount is that will make sure your taxes are covered on tax day. You do not need to worry about a set amount.

Do I have to pay the same amount every quarter?

The IRS does prefer the same amount each quarter. However, if your income differs dramatically from one quarter to the next, they make allowances. Ultimately they prefer your payments be proportional to your income and do not want estimated tax payments back loaded to the end of the year.

When are quarterly payments due?

The typical quarterly payment dates are April 15, June 15, September 15, and January 15. Dates change slightly when those dates land on weekends. First and Second quarter payments in 2020 were made due in July 2020 due to the pandemic, however drastic changes like that are rare.